Last updated on June 11th, 2023 at 08:31 am

Cleaning Up your Credit

Here’s how to clean up your credit so you get the least-expensive home loan possible.

Getting the loan that suits your situation at the best possible price and terms makes home-buying easier and more affordable. Here are seven ways to boost your credit score so you can do just that.

1. Know your credit score

Credit scores range from 300 to 850, and the higher, the better. They’re based on whether you’ve paid personal loans, car loans, credit cards, and other debt in full and on time in the past. You’ll need a score of at least 620 to qualify for a home loan and 740 to get the best interest rates and terms.

You’re entitled to a free copy of your credit report annually from each of the major credit-reporting bureaus, Equifax (http://www.equifax.com), Experian (http://www.experian.com), and TransUnion (http://www.transunion.com). Access all three versions of your credit report at (http://www.annualcreditreport.com). Review them to ensure the information is accurate.

2. Correct errors on your credit report

If you find mistakes on your credit report, write a letter to the credit-reporting agency explaining why you believe there’s an error. Send documents that support your case, and ask that the error is corrected or removed. Also, write to the company, or debt collector, that reported the incorrect information to dispute the information and ask to be copied on any materials sent to credit-reporting agencies.

3. Pay every bill on time

You may be surprised at the damage even a few late payments will have on your credit score. The easiest way to make a big difference in your credit score without altering your spending habits is to diligently pay all your bills on time. You’ll also save money because you’ll keep the money you’ve been spending on late fees. Credit card or mortgage companies probably won’t report minor late payments, those less than 30 days overdue, but you’ll still have to pay late fees.

4. Use credit carefully

Another good way to boost your credit score is to pay your credit card bills in full every month. If you can’t do that, pay as much over your required minimum payment as possible to begin whittling away the debt. Stop using your credit cards to keep your balances from increasing, and transfer balances from high-interest credit cards to lower-interest cards.

5. Take care with the length of your credit

Credit rating agencies also consider the length of your credit history. If you’ve had a credit card for a long time and managed it responsibly, that works in your favor. However, opening several new credit cards at once can lower the average age of your accounts, which pushes down your score. Likewise, closing credit card accounts lowers your available credit, so keep credit cards open even if you’re not using them.

6. Don’t use all the credit you’re offered

Credit scores are also based on how much credit you use compared with how much you’re offered. Using $1,000 of available credit will give you a lower score than having $1,000 of available credit and using $100 of it. Occasionally opening new lines of credit can boost your available credit, which also affects your score positively.

7. Be patient

It can take time for your credit score to climb once you’ve begun working to improve it. Keep at it because the more distance you put between your spotty payment history and your current good payment record, the less damage you’ll do to your credit score.

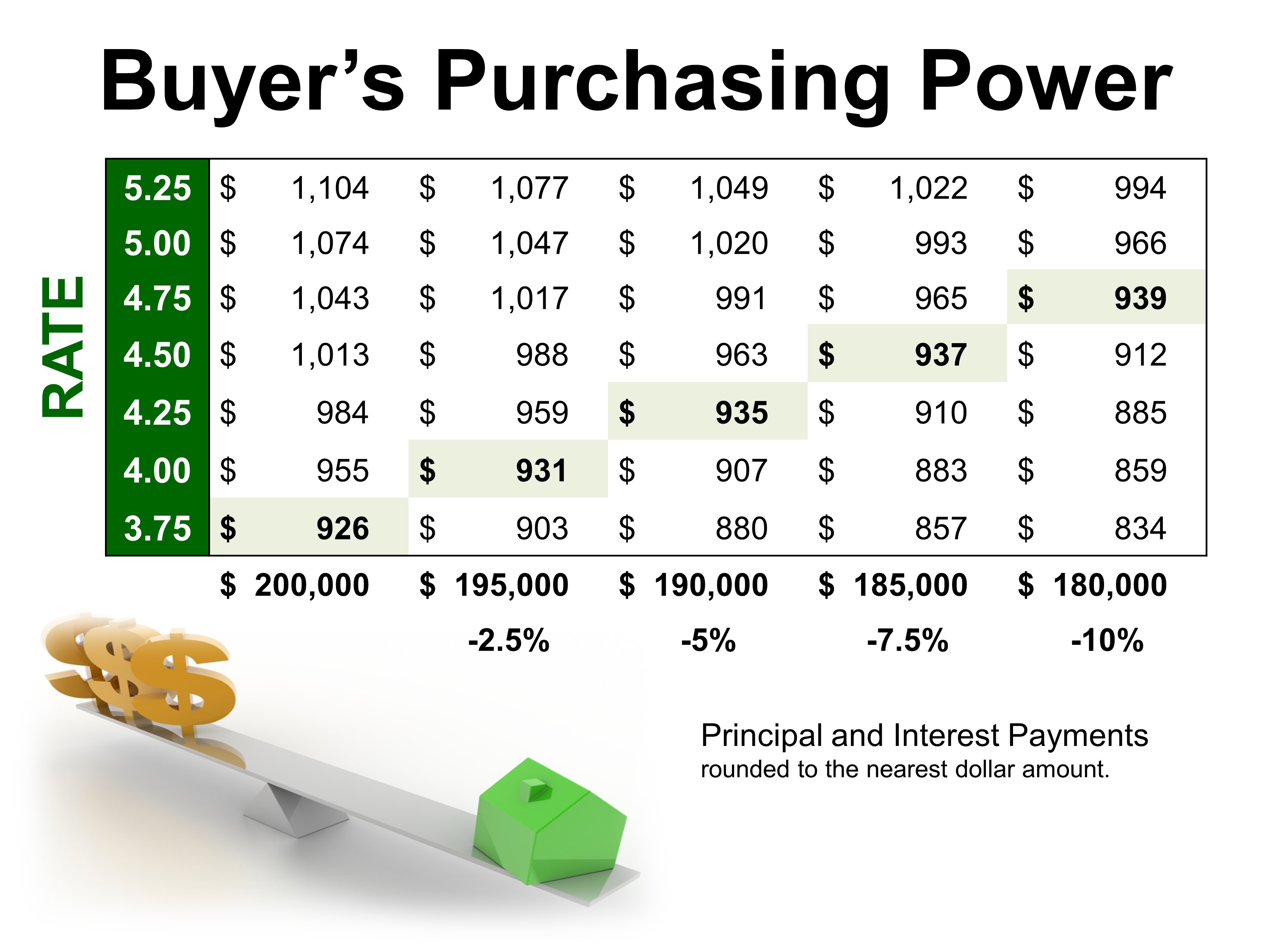

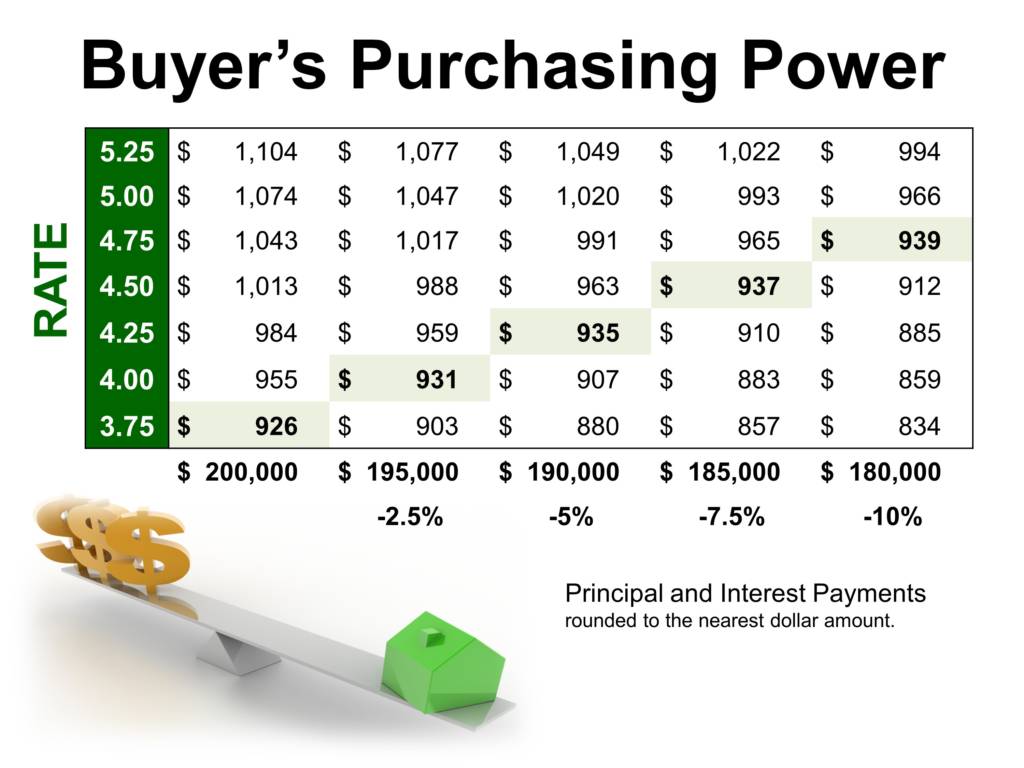

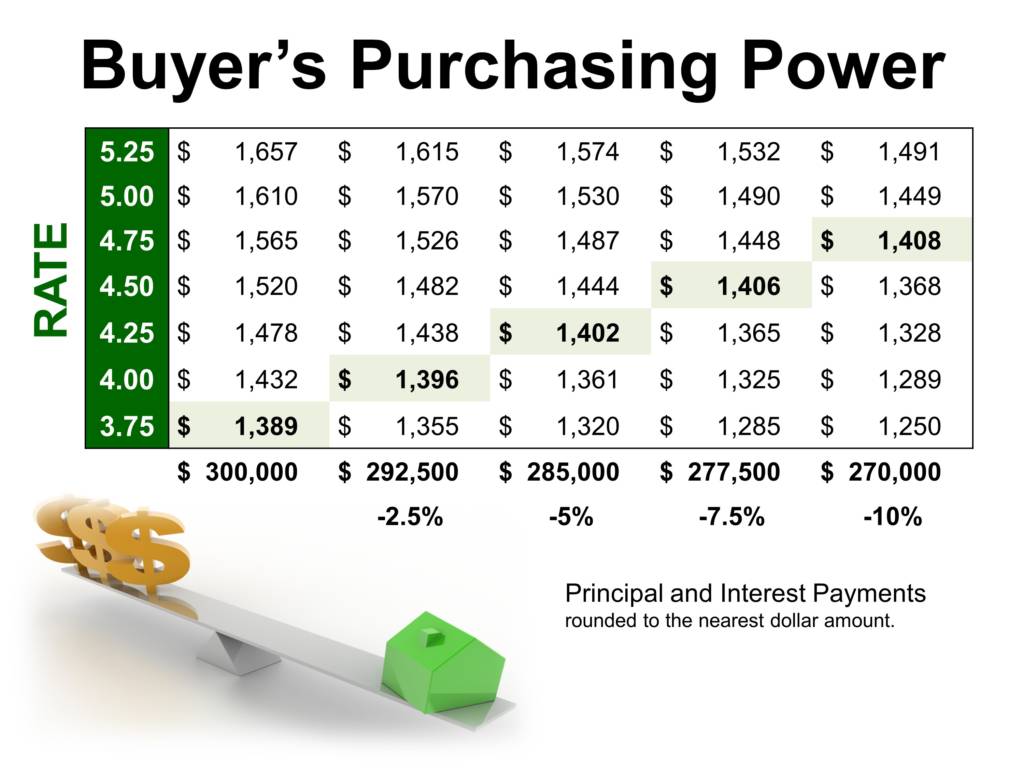

One of the best reasons to want to have the best credit score possible is that it affects the interest rate you will be charged on a mortgage. Seeing how that affects your buying power is amazing!

Other web resources

How FICO scores are calculated (http://www.myfico.com/CreditEducation/WhatsInYourScore.aspx)

Answers to frequently asked credit report questions (https://www.annualcreditreport.com/cra/helpfaq)

The bulk of the information provided by!

G.M. Filisko is an attorney and award-winning writer who keeps a close eye on her credit scores. A frequent contributor to many national publications including Bankrate.com, REALTOR? Magazine, and the American Bar Association Journal, she specializes in real estate, business, personal finance, and legal topics.

For More Home Buying Tips!

Be sure to check out our Home Buyers Section:

And Our Real Estate Contracts Section so you learn in advance what you will be signing.